What Is the 50/30/20 Budgeting Rule?

What Is the 50/30/20 Budgeting Rule?

Managing money effectively can feel complicated, especially with endless expenses, financial goals, and unexpected costs. Yet one of the simplest and most effective frameworks for personal finance is the 50/30/20 budgeting rule. This rule offers an easy way to balance your spending, saving, and debt repayment — helping you live within your means while still planning for the future.

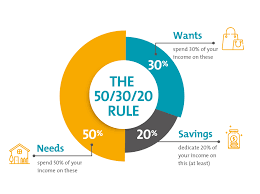

In essence, the 50/30/20 rule divides your after-tax income into three categories:

-

50% for needs

-

30% for wants

-

20% for savings and debt repayment

It’s a flexible, intuitive system that can be adapted to nearly any income level or lifestyle.

The Origin of the 50/30/20 Rule

The 50/30/20 rule became widely known through the book “All Your Worth: The Ultimate Lifetime Money Plan” by U.S. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi. The authors designed this approach to simplify budgeting and make financial planning accessible to everyone — not just experts or high earners.

Rather than tracking every small expense, the 50/30/20 rule provides a big-picture structure that ensures you’re covering essential needs, enjoying life, and saving responsibly.

Understanding the 50/30/20 Breakdown

Let’s explore what each category includes and how to apply it in real life.

1. 50%: Needs

Your “needs” are essential expenses — the costs you must pay to live and work. These are non-negotiable items that maintain your basic standard of living.

Examples of needs include:

-

Rent or mortgage payments

-

Utilities (electricity, water, gas)

-

Transportation (fuel, car payments, public transit)

-

Insurance (health, auto, home)

-

Minimum debt payments

-

Groceries (basic food items)

-

Childcare and essential healthcare

If your needs exceed 50% of your income, it may be a sign that your living situation or financial commitments need adjustment — such as downsizing housing, refinancing loans, or finding cheaper service providers.

2. 30%: Wants

“Wants” are the things that make life more enjoyable but aren’t strictly necessary. They’re important for maintaining motivation, happiness, and quality of life — but they should be controlled to avoid overspending.

Examples of wants include:

-

Dining out and takeout meals

-

Entertainment (streaming services, movies, concerts)

-

Vacations and travel

-

Hobbies and leisure activities

-

Fashion and luxury items

-

Upgraded technology (new phones, gadgets)

Balancing wants is crucial — you don’t need to eliminate enjoyment entirely, but being mindful ensures your lifestyle doesn’t undermine your financial health.

3. 20%: Savings and Debt Repayment

The final 20% of your income should go toward building financial security — saving for the future and paying down debt faster.

Examples include:

-

Contributions to emergency funds

-

Retirement savings (401(k), IRA, pension plans)

-

Investments (stocks, mutual funds)

-

Extra payments on loans or credit cards

-

Saving for long-term goals (home purchase, education, etc.)

This category ensures that you’re not just living for today, but preparing for tomorrow.

Why the 50/30/20 Rule Works

The brilliance of the 50/30/20 rule lies in its simplicity and flexibility. It doesn’t require tracking every dollar or using complex financial tools. Instead, it provides an easy-to-follow roadmap that helps maintain balance and discipline.

Key Benefits:

-

Simple and clear: You only need to track three spending categories.

-

Promotes financial balance: Ensures you’re not overspending on wants or neglecting savings.

-

Adaptable: Works for most income levels and lifestyles.

-

Encourages mindfulness: Helps you evaluate what truly matters in your spending.

-

Builds long-term stability: Regular saving and debt reduction create financial freedom over time.

How to Implement the 50/30/20 Rule

Here’s a step-by-step guide to applying this rule to your finances:

Step 1: Calculate Your After-Tax Income

Start by identifying your take-home pay — the amount left after taxes and deductions.

-

If you’re an employee, use your net paycheck amount.

-

If you’re self-employed, subtract taxes, business expenses, and contributions before applying the rule.

Step 2: Categorize Your Expenses

List all your monthly expenses and group them into needs, wants, and savings/debt repayment categories. This helps you see where your money currently goes.

For example:

-

Needs: $2,500

-

Wants: $1,000

-

Savings/Debt: $500

If these don’t align with the 50/30/20 proportions, you can begin adjusting gradually.

Step 3: Adjust and Set Goals

If your needs exceed 50%, consider ways to cut costs — such as renegotiating bills, reducing rent, or switching to a cheaper car.

If your wants take up more than 30%, identify discretionary spending to trim.

And if your savings are less than 20%, automate transfers to make saving effortless.

Step 4: Automate Your Finances

Automation is key to staying consistent. Set up automatic transfers to savings or investment accounts right after payday. This way, saving becomes a habit — not an afterthought.

Step 5: Revisit Regularly

Your financial situation changes over time. Review your budget every few months or after major life events (new job, relocation, family changes) to ensure your allocations still make sense.

Example: Applying the Rule

Imagine your after-tax monthly income is $4,000. Here’s how you might allocate it:

| Category | Percentage | Amount | Examples |

|---|---|---|---|

| Needs | 50% | $2,000 | Rent, groceries, utilities, transportation, insurance |

| Wants | 30% | $1,200 | Dining out, subscriptions, hobbies, travel |

| Savings & Debt | 20% | $800 | Emergency fund, investments, loan overpayments |

This structure provides a balanced approach — covering essentials, allowing enjoyment, and building long-term stability.

Adapting the 50/30/20 Rule to Your Situation

While the 50/30/20 split is a helpful guideline, it’s not one-size-fits-all. Different financial stages, locations, and goals may require tweaking the ratios.

1. High Cost of Living Areas

If you live in an expensive city, housing and transportation might exceed 50%. In that case, you might use a 60/20/20 or 70/20/10 approach until your income grows.

2. Aggressive Savings Goals

If you’re saving for a house, retiring early, or paying off debt quickly, you might shift to a 40/20/40 plan — reducing wants to increase savings.

3. Variable Income

Freelancers or commission-based workers can base percentages on an average income or use flexible budgeting — prioritizing needs first, then distributing remaining funds between wants and savings.

The beauty of this rule lies in its adaptability — you can mold it to fit your financial priorities without losing its core principles.

Common Mistakes to Avoid

While the 50/30/20 rule is simple, a few pitfalls can undermine its effectiveness:

-

Misclassifying expenses: Calling luxury items “needs” can distort your budget. Be honest with yourself.

-

Ignoring irregular costs: Don’t forget annual expenses like insurance premiums or car maintenance.

-

Neglecting to review: Over time, lifestyle creep (gradually spending more as you earn more) can disrupt your balance.

-

Not automating savings: Relying on willpower alone often leads to skipped savings.

-

Underestimating debt repayment: Only paying minimums may extend debt for years. Aim to allocate more when possible.

How It Compares to Other Budgeting Methods

There are several budgeting systems out there — but the 50/30/20 rule stands out for its ease of use. Here’s how it compares:

| Method | Description | Pros | Cons |

|---|---|---|---|

| Zero-Based Budgeting | Every dollar has a purpose; income minus expenses = 0 | Extremely detailed; full control | Time-consuming to maintain |

| Envelope System | Cash divided into envelopes for categories | Encourages discipline | Inconvenient for digital payments |

| Pay Yourself First | Prioritize savings before spending | Builds wealth automatically | May ignore spending balance |

| 50/30/20 Rule | Simplifies money into 3 key categories | Easy, flexible, balanced | Less detailed for complex finances |

If you’re new to budgeting, the 50/30/20 method is a perfect place to start before exploring more advanced techniques.

Digital Tools to Help You Apply the Rule

Many budgeting apps and tools make it easier to follow the 50/30/20 rule automatically.

Some popular options include:

-

Mint – Tracks spending and categorizes transactions automatically.

-

You Need a Budget (YNAB) – Great for goal-setting and real-time awareness.

-

Empower (formerly Personal Capital) – Combines budgeting with investment tracking.

-

Simplifi by Quicken – Offers visual breakdowns that align with the 50/30/20 approach.

Even a simple spreadsheet or notes app can work — the key is consistency.

Why Saving and Debt Repayment Matter Most

The 20% allocation is the cornerstone of long-term financial security. It builds your financial resilience and freedom by addressing both short-term emergencies and long-term goals.

1. Emergency Fund

Having 3–6 months of living expenses saved protects you from job loss, medical bills, or unexpected repairs.

2. Debt Reduction

Paying off high-interest debt (like credit cards) can save you thousands in the long run and reduce financial stress.

3. Retirement Savings

Contributing to retirement accounts early allows your money to grow through compound interest — one of the most powerful forces in personal finance.

4. Investment Growth

Once you’ve built an emergency fund and reduced debt, investing helps your money work for you — growing faster than traditional savings.

When the 50/30/20 Rule May Not Fit Perfectly

While effective, this rule may need adjustment in certain situations:

-

Low income or high debt: You might need to allocate more than 20% to debt repayment temporarily.

-

Unpredictable income: Freelancers may need to set aside a portion for taxes before applying the rule.

-

Families with dependents: Childcare or healthcare may inflate “needs” beyond 50%.

That’s okay — the point isn’t perfection, but progress and awareness.

Tips for Sticking to the Rule Long-Term

-

Track your progress monthly. Use apps or spreadsheets to stay on top of categories.

-

Automate savings. Treat saving like a fixed expense.

-

Plan for fun. Budgeting shouldn’t feel restrictive — schedule “want” spending guilt-free.

-

Adjust as you grow. Update your percentages as income or goals change.

-

Reward yourself. Celebrate milestones, like paying off debt or reaching savings targets.

The Bottom Line

The 50/30/20 budgeting rule is more than just a formula — it’s a mindset. It helps you align your spending with your values, live within your means, and steadily build financial security.

By committing 50% of your income to essentials, 30% to personal enjoyment, and 20% to savings and debt repayment, you can create balance and peace of mind. Whether you’re starting your first job, managing a family budget, or recovering from financial setbacks, this framework provides clarity and structure.

Ultimately, financial success doesn’t come from perfection — it comes from consistency. The 50/30/20 rule makes that consistency achievable for anyone.

- Arts

- Business

- Computers

- Giochi

- Health

- Home

- Kids and Teens

- Money

- News

- Personal Development

- Recreation

- Regional

- Reference

- Science

- Shopping

- Society

- Sports

- Бизнес

- Деньги

- Дом

- Досуг

- Здоровье

- Игры

- Искусство

- Источники информации

- Компьютеры

- Личное развитие

- Наука

- Новости и СМИ

- Общество

- Покупки

- Спорт

- Страны и регионы

- World