What is behavioral economics?

What Is Behavioral Economics? The Discipline That Discovered How We Actually Decide

The Mistake That Changed Economics

Several years ago, I found myself standing in a grocery store, holding two bottles of wine.

One cost $12. The other cost $24.

I knew almost nothing about wine. Yet I lingered. I examined labels I did not understand, regions I could not locate on a map, and tasting notes that might as well have been poetry. Then I purchased the more expensive bottle.

Not because I expected it to taste twice as good. Not because I had performed a careful analysis. And certainly not because I possessed specialized knowledge.

I bought it because the higher price seemed to signal quality.

Later that evening, a friend who knew considerably more about wine informed me that my choice revealed less about wine than about human judgment.

The observation stayed with me.

Traditional economics would describe my decision as a rational attempt to maximize value. Behavioral economics asks a more unsettling question: What if the story I tell myself about my decision is incomplete? What if the real causes lie beneath conscious awareness?

This question sits at the center of one of the most influential intellectual movements of the past half-century.

Behavioral economics emerged from a simple but disruptive insight: human beings are not the perfectly rational decision-makers imagined by classical economic theory. We are systematic thinkers, but not always logical ones. We are capable of extraordinary reasoning, yet vulnerable to predictable errors. We calculate, estimate, compare, and forecast—but often in ways that depart from objective reality.

The field transformed economics by importing lessons from psychology. In doing so, it revealed that irrationality is not random. It follows patterns.

And patterns can be studied.

What Is Behavioral Economics?

Behavioral economics is the study of how psychological, emotional, cognitive, and social factors influence economic decisions.

Unlike traditional economics, which assumes that individuals consistently act in their own best interests, behavioral economics examines how people actually behave when confronted with uncertainty, risk, temptation, and complexity.

The discipline investigates questions such as:

-

Why do investors panic during market declines?

-

Why do consumers spend more with credit cards than cash?

-

Why do people purchase extended warranties that rarely pay off?

-

Why do employees fail to enroll in retirement plans even when doing so would clearly benefit them?

-

Why does the wording of a choice affect the choice itself?

The answers often reveal a gap between intention and action.

Behavioral economics is not merely the study of mistakes. It is the study of the architecture of judgment.

The Traditional Economic Model: Elegant, Useful, and Incomplete

For much of the twentieth century, economics relied on a powerful simplifying assumption.

Individuals were treated as rational agents.

This hypothetical person—sometimes called Homo economicus—possessed stable preferences, complete information, and unlimited computational ability. Presented with alternatives, he would weigh costs and benefits and select the option that maximized utility.

The model produced remarkable insights.

It enabled economists to explain markets, prices, incentives, competition, and resource allocation. Much of modern economic theory rests upon it.

Yet there was always a tension.

Real people did not resemble the model.

Consumers purchased products they did not need. Investors chased speculative bubbles. Voters supported policies that conflicted with their stated interests. Workers procrastinated. Shoppers succumbed to impulse purchases. Managers became overconfident.

The discrepancy was impossible to ignore.

Behavioral economics emerged from this tension between elegant theory and messy reality.

The Psychological Revolution in Economics

The roots of behavioral economics lie in psychology.

During the 1970s, psychologists began documenting systematic departures from rational judgment. Their experiments demonstrated that people rely on mental shortcuts—heuristics—that often work remarkably well but occasionally produce predictable errors.

The findings accumulated.

People overestimated rare events.

They underestimated uncertainty.

They became attached to possessions they already owned.

They reacted differently to identical outcomes depending on how choices were framed.

One experiment after another challenged assumptions about human rationality.

The significance was not that people sometimes made mistakes. That had always been obvious.

The significance was that the mistakes were systematic.

They appeared repeatedly across cultures, contexts, and populations.

Once economists recognized these patterns, a new field became inevitable.

System 1 and System 2: The Two Minds Within Us

One of the most useful frameworks for understanding behavioral economics is the distinction between two modes of thinking.

System 1: Fast Thinking

System 1 operates automatically.

It recognizes faces.

It completes familiar phrases.

It generates impressions.

It detects threats.

It produces intuitive judgments with remarkable speed.

Most of the time, it serves us well.

Without it, everyday life would become impossible.

Yet speed has a cost.

System 1 often substitutes easy questions for difficult ones.

Instead of asking, “What is the statistical probability?” it asks, “What comes to mind most easily?”

Instead of asking, “What does the evidence suggest?” it asks, “How do I feel about this?”

The substitution occurs silently.

System 2: Slow Thinking

System 2 is deliberate and analytical.

It performs calculations.

It evaluates arguments.

It compares alternatives.

It examines evidence.

System 2 is capable of correcting System 1.

The problem is that it frequently declines the invitation.

Careful thinking requires effort. Human beings are, by nature, cognitive misers. We conserve mental energy whenever possible.

As a result, many economic decisions originate not from deliberate calculation but from intuitive impressions.

This insight lies at the heart of behavioral economics.

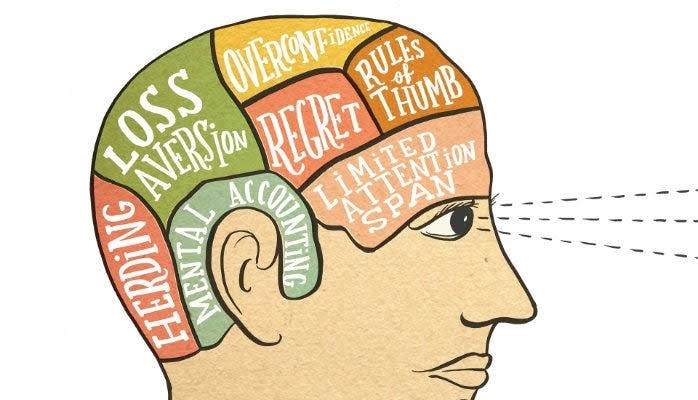

The Most Important Concepts in Behavioral Economics

Loss Aversion

Imagine receiving $100 unexpectedly.

You would probably feel pleased.

Now imagine losing $100 from your wallet.

The emotional impact would likely be stronger.

This asymmetry is known as loss aversion.

Losses hurt more than equivalent gains feel good.

Researchers repeatedly find that the psychological pain of losing often exceeds the pleasure of gaining by a substantial margin.

Loss aversion helps explain why:

-

Investors hold losing stocks too long.

-

Consumers resist price increases.

-

Employees dislike reductions in benefits.

-

Homeowners overvalue their properties.

Economic outcomes are not evaluated in absolute terms. They are experienced psychologically.

And psychology has its own arithmetic.

Anchoring

Suppose someone asks whether the population of a city exceeds one million people.

Afterward, they ask you to estimate the actual population.

The initial number influences your estimate, even if it is arbitrary.

This phenomenon is called anchoring.

The mind latches onto a reference point and adjusts insufficiently.

Anchoring affects:

-

Salary negotiations

-

Retail pricing

-

Real estate transactions

-

Legal judgments

-

Consumer purchasing decisions

A shirt marked down from $200 to $80 appears attractive partly because the original price serves as an anchor.

The anchor shapes perception.

The objective value becomes secondary.

Availability Bias

People estimate probability according to how easily examples come to mind.

If airplane crashes dominate news coverage, flying feels dangerous.

If stories about lottery winners are memorable, winning appears more plausible than it truly is.

The ease of recall becomes a substitute for statistical frequency.

This shortcut is efficient.

It is also frequently misleading.

Media attention often amplifies rare events while obscuring common ones.

As a result, public fears and actual risks can diverge dramatically.

Confirmation Bias

Once individuals form a belief, they naturally seek evidence that supports it.

Contradictory information receives less attention.

Supporting information feels persuasive.

This tendency appears in politics, investing, business strategy, and personal relationships.

Confirmation bias does not arise because people dislike truth.

It arises because coherence feels comfortable.

The mind prefers consistency over uncertainty.

The Endowment Effect

Ownership changes perception.

People tend to assign greater value to objects merely because they possess them.

A coffee mug owned for five minutes becomes more valuable than an identical mug sitting on a store shelf.

The effect appears irrational from a market perspective.

Yet psychologically it makes sense.

Giving up something already owned feels like a loss.

And losses loom large.

A Comparison: Traditional Economics vs. Behavioral Economics

| Dimension | Traditional Economics | Behavioral Economics |

|---|---|---|

| View of Human Nature | Rational and self-interested | Predictably imperfect |

| Decision Process | Logical optimization | Mix of intuition and analysis |

| Information Processing | Complete and objective | Limited and biased |

| Preferences | Stable and consistent | Context-dependent |

| Risk Assessment | Statistically rational | Influenced by emotion |

| Market Behavior | Efficient outcomes dominate | Biases can persist |

| Consumer Choices | Utility maximizing | Influenced by framing and heuristics |

| Policy Design | Incentives alone matter | Choice architecture matters |

| Errors | Random and self-correcting | Systematic and predictable |

| Research Foundation | Mathematics and theory | Economics plus psychology |

The distinction is not absolute.

Behavioral economics does not reject traditional economics.

Rather, it extends it.

Classical models remain useful.

Behavioral insights help explain where those models break down.

Why Smart People Make Predictable Mistakes

One of the most surprising lessons of behavioral economics is that intelligence offers less protection than many assume.

Experts are vulnerable.

Executives are vulnerable.

Professors are vulnerable.

Judges are vulnerable.

Experience often improves knowledge without eliminating bias.

Indeed, expertise occasionally creates a dangerous illusion of certainty.

The issue is not lack of intelligence.

The issue is architecture.

Human cognition evolved to operate quickly in uncertain environments, not to solve abstract statistical problems.

Many biases emerge from mechanisms that generally serve us well.

The same intuition that enables rapid decision-making can also generate error.

The same confidence that supports action can produce overconfidence.

The same pattern recognition that detects opportunities can discover patterns that do not exist.

Behavioral economics studies these tradeoffs.

How Businesses Use Behavioral Economics

Organizations increasingly apply behavioral insights to influence consumer behavior.

Some applications are benign.

Others raise ethical questions.

Pricing Strategies

Retailers use anchors to shape perceptions of value.

A product listed at $500 and discounted to $299 appears more attractive than a product introduced directly at $299.

The reference point matters.

Subscription Models

Many subscription services rely on inertia.

Customers intend to cancel.

They postpone.

Automatic renewal becomes the default.

Behavior fills the gap between intention and action.

Choice Architecture

The arrangement of options influences decisions.

A cafeteria placing fruit at eye level often increases healthy food purchases.

Nothing is forbidden.

No incentives change.

The environment changes.

Behavior follows.

The Rise of the “Nudge”

Perhaps the most influential practical application of behavioral economics is the concept of the nudge.

A nudge alters behavior without restricting freedom of choice.

Consider retirement savings.

Many employees intend to enroll in workplace retirement plans.

Many fail to do so.

Traditional economics interprets this as a deliberate choice.

Behavioral economics suspects procrastination.

The solution is simple.

Instead of requiring employees to opt in, organizations automatically enroll them while preserving the option to opt out.

Participation rates frequently rise dramatically.

No one is forced.

Yet outcomes improve.

This principle has influenced public policy around the world.

Governments now use behavioral insights to improve tax compliance, increase organ donor participation, reduce energy consumption, and encourage healthier lifestyles.

The Limits of Behavioral Economics

Like every intellectual framework, behavioral economics has limitations.

Some advocates occasionally treat irrationality as universal.

This is an exaggeration.

People often behave remarkably rationally.

Markets frequently discipline errors.

Experience matters.

Learning occurs.

Not every deviation from a model reflects a cognitive bias.

Sometimes individuals possess information researchers do not.

Sometimes seemingly irrational behavior reflects reasonable tradeoffs.

The challenge is maintaining balance.

Behavioral economics is most powerful when viewed as a supplement rather than a replacement for traditional theory.

Human beings are neither perfectly rational nor hopelessly irrational.

We inhabit the space between.

A Lesson I Learned About Decision-Making

Years ago, I became convinced that a particular project would succeed.

The evidence seemed compelling.

Every conversation reinforced my confidence.

Every article appeared supportive.

Every forecast aligned with my expectations.

The project failed.

Only afterward did I recognize what had happened.

I had not been evaluating evidence.

I had been collecting confirmation.

Information that supported my conclusion felt persuasive. Information that challenged it felt flawed.

The distinction became visible only in retrospect.

That experience altered how I make decisions.

I now pay particular attention to evidence that makes me uncomfortable. I ask what would have to be true for my conclusion to be wrong. I seek disagreement rather than affirmation.

These habits do not eliminate bias.

Nothing does.

But they create friction between intuition and action.

Behavioral economics teaches that judgment improves not when we trust ourselves completely, but when we understand the limits of trust.

Why Behavioral Economics Matters More Than Ever

Modern life presents an unusual challenge.

Individuals now make more decisions than previous generations and make them under conditions of extraordinary complexity.

Financial products contain hundreds of pages of disclosures.

Online marketplaces offer endless alternatives.

Investment opportunities appear continuously.

Information arrives faster than attention can process it.

Under such conditions, mental shortcuts become indispensable.

Yet the environments in which those shortcuts evolved differ dramatically from today's world.

The result is a growing mismatch between ancient cognitive machinery and modern decision environments.

Behavioral economics provides a map of that mismatch.

It reveals where intuition excels and where it falters.

It helps explain why consumers overspend, investors overreact, voters misjudge probabilities, and organizations cling to failing strategies.

Most importantly, it offers practical tools for improvement.

Not perfection.

Improvement.

Conclusion: The Uncomfortable Truth About Human Rationality

Behavioral economics begins with a modest observation and ends with a profound implication.

The observation is that people do not always choose rationally.

The implication is that our understanding of ourselves may be less reliable than we imagine.

We like to believe our decisions emerge from careful reasoning. We prefer stories in which judgment follows evidence and action follows logic.

Reality is more complicated.

Much of what guides behavior occurs automatically. Context matters. Framing matters. Defaults matter. Ownership matters. Losses matter.

Small details often exert large effects.

This realization can feel unsettling. Yet there is something liberating about it as well.

If our errors were random, improvement would be difficult. But behavioral economics demonstrates that many errors are predictable. Patterns can be recognized. Systems can be redesigned. Decisions can be structured more intelligently.

The discipline does not tell us that humans are irrational creatures stumbling through life blindly.

Its message is subtler.

We are reasoning beings equipped with imperfect tools. Those tools are astonishingly powerful, occasionally deceptive, and endlessly fascinating.

Understanding them may be one of the most important economic investments we can make.

- Arts

- Business

- Computers

- Jogos

- Health

- Início

- Kids and Teens

- Money

- News

- Personal Development

- Recreation

- Regional

- Reference

- Science

- Shopping

- Society

- Sports

- Бизнес

- Деньги

- Дом

- Досуг

- Здоровье

- Игры

- Искусство

- Источники информации

- Компьютеры

- Личное развитие

- Наука

- Новости и СМИ

- Общество

- Покупки

- Спорт

- Страны и регионы

- World