What Percentage of My Salary Should Go to Savings? Budgeting Frameworks Explained

What Percentage of My Salary Should Go to Savings? Budgeting Frameworks Explained

Figuring out how much of your salary should go to savings can feel overwhelming, especially when budgets are tight, income fluctuates, or financial goals seem far away. Yet this single decision—how much you save—often has the greatest impact on long-term stability, opportunity, and peace of mind.

There’s no one-size-fits-all percentage, but there are proven budgeting frameworks and principles that can guide you. This article breaks down the most trusted models—including the popular 50/30/20 rule—while helping you decide what’s realistic for your lifestyle and goals.

Why Savings Percentages Matter

Savings is often the most postponed line in a budget. Housing, transportation, groceries, healthcare, and daily life get priority—leaving savings as whatever’s “left over.” But reversing this mindset is key to building financial resilience.

A savings percentage gives you:

-

Predictability: You treat saving as a fixed “bill,” not an optional leftover.

-

Goal alignment: You know if you’re on track for your emergency fund, big purchases, investments, or retirement.

-

Adaptability: Even when income changes, the proportional model automatically adjusts.

The right percentage helps you build wealth intentionally instead of accidentally.

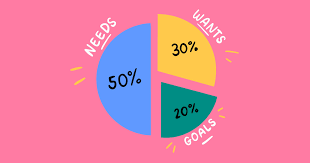

The 50/30/20 Framework: A Timeless Starting Point

The 50/30/20 rule, popularized by Senator Elizabeth Warren, is one of the most commonly recommended budgeting frameworks. It divides your take-home pay into three simple categories:

-

50% — Needs

Rent/mortgage, utilities, groceries, insurance, transportation, minimum debt payments. -

30% — Wants

Restaurants, hobbies, subscriptions, entertainment, nonessential shopping. -

20% — Savings and debt acceleration

Emergency fund, retirement contributions, investments, and extra loan payments.

How Much of That is Actual Savings?

The 20% category typically includes:

-

10–15% retirement contributions

-

5–10% cash savings or investments

-

Any extra debt payments

In practice, this usually means 10–20% of your take-home pay goes directly toward savings.

Who the 50/30/20 Rule Works Best For

-

Early-career earners who need a simple starting structure

-

People with average cost of living and stable income

-

Anyone overwhelmed by complex budgeting systems

If you have no current savings plan, 50/30/20 is an excellent first framework.

Other Budgeting Frameworks for Different Lifestyles

The 60/30/10 Rule

A more flexible approach:

-

60% Needs

-

30% Wants

-

10% Savings

Best for:

-

High cost-of-living areas

-

Those with tight budgets or large fixed expenses

Savings is lower at 10%, but consistency still matters.

The 70/20/10 Rule

Common among people with high expenses or debt:

-

70% Living expenses (needs + wants combined)

-

20% Savings and investments

-

10% Debt repayment or giving

This preserves a solid 20% for savings-only goals.

The 80/20 Rule (“Pay Yourself First”)

Simple and effective:

-

20% Savings

-

80% Expenses

This minimalist rule is ideal for people who want savings automated without micro-budgeting.

The 40% Rule for High Earners

As income rises, expenses don’t have to keep pace. Many financial planners recommend:

-

40% Taxes

-

40% Savings or investments

-

20% Expenses

Suitable for:

-

High-income earners (especially without children)

-

Those pursuing early retirement (FIRE movement)

So What Percentage Should You Save? (Based on Life Stage)

If You’re in Your 20s

Recommended: 10–20% of income

Start small but start early. Compounding does most of the heavy lifting.

If You’re in Your 30s

Recommended: 15–25%

This is when long-term goals—buying a home, raising kids, investing—are front and center.

If You’re in Your 40s

Recommended: 20–30%

If retirement savings started late, this is the catch-up stage.

If You’re in Your 50s and Beyond

Recommended: 25–35%

This depends heavily on retirement readiness, but most need to increase contributions.

How to Determine Your Personal Savings Percentage

Ask yourself these five questions to find the right number:

1. Do I have an emergency fund?

-

Less than 1 month saved → prioritize savings (15–25%)

-

1–3 months saved → aim for 10–20%

-

3–6 months saved → maintain or shift toward investing

2. What are my financial goals?

Savings aligns with goals, not guesswork.

Common targets:

-

Buying a home

-

Travel or big purchases

-

Wedding

-

Education

-

Early retirement

-

Starting a business

Larger goals require a higher savings percentage.

3. Am I paying high-interest debt?

If credit cards or personal loans exceed 8–10% interest, allocate part of your “savings” bucket toward debt acceleration. You're still improving net worth.

4. What’s my cost of living?

-

High COL → 10–15% savings may be more realistic

-

Low COL → 20–30% is often achievable

5. What’s my income stability?

-

Freelancers or contractors may need 20–30%

-

Stable, salaried workers can aim for 10–20%

How to Start Saving If Money Is Tight

Even if the recommended percentages feel impossible, you can build the habit gradually.

Start with micro-percentages

-

1% this month

-

2% next month

-

Keep increasing until you reach your target

Automate everything

Savings should leave your account before you see it.

Cut lifestyle creep

When income increases, raise your savings percentage—not your spending.

Use separate accounts

One for long-term goals, one for emergencies, one for daily spending.

Track your progress monthly

Most people overestimate their needs and underestimate their wants.

A Realistic Breakdown for Different Salary Levels

If you earn $35,000–$50,000

Aim for 10–15% savings and optimize for emergency funds and debt reduction.

If you earn $50,000–$75,000

Aim for 15–20%, balancing retirement and personal goals.

If you earn $75,000–$150,000

Aim for 20–30%, especially for investment growth and future financial independence.

If you earn $150,000+

Consider 25–40% savings, depending on lifestyle and retirement ambitions.

How Taxes Influence Your Savings Percentage

If you contribute to retirement accounts like 401(k), IRA, or other pre-tax vehicles, remember:

-

Pre-tax contributions increase your effective savings rate

-

They may allow you to “save more” while keeping take-home pay stable

This means someone contributing 10% to a 401(k) may already be close to the recommended 15–20% savings once taxes are factored in.

Should You Save More If You Want to Retire Early?

Yes. Early retirement frameworks, like FIRE (Financial Independence, Retire Early), commonly use these savings ranges:

-

25% savings rate → retire in ~32 years

-

40% savings rate → retire in ~20 years

-

60% savings rate → retire in ~12 years

Your savings rate is the biggest driver of early financial independence.

What If You Can’t Hit Any of These Numbers?

That’s completely normal. Many people cannot start with double-digit savings.

Here’s what matters most:

-

Save something—even 1%.

-

Increase slowly and consistently.

-

Avoid the trap of all-or-nothing thinking.

-

Automate your increases (like retirement auto-escalation).

The habit is more important than the initial amount.

The Bottom Line: The “Right” Savings Percentage

There is no universal perfect number—but there is a general guideline:

Most people should aim to save 15–20% of their take-home pay.

This aligns with:

-

The 50/30/20 rule

-

Retirement planning projections

-

Growth-oriented financial frameworks

But depending on your situation, anywhere from 10% to 30% can be reasonable and effective.

If you’re unsure where to begin, start small, follow a simple framework, and adjust over time. The key is consistency—not perfection.

Saving isn’t about depriving yourself; it’s about giving your future self options, security, and freedom. And the earlier you start, the more powerful those options become.

- Arts

- Business

- Computers

- Giochi

- Health

- Home

- Kids and Teens

- Money

- News

- Personal Development

- Recreation

- Regional

- Reference

- Science

- Shopping

- Society

- Sports

- Бизнес

- Деньги

- Дом

- Досуг

- Здоровье

- Игры

- Искусство

- Источники информации

- Компьютеры

- Личное развитие

- Наука

- Новости и СМИ

- Общество

- Покупки

- Спорт

- Страны и регионы

- World