What is business cycle theory?

The Quiet Logic Behind Economic Turbulence

There is a peculiar regularity to economic disorder. Booms feel euphoric, busts feel catastrophic, yet—seen from a distance—they trace patterns that are almost unsettling in their familiarity. The same sequence repeats: expansion, overheating, contraction, recovery. It is tempting to interpret these swings as failures of foresight or lapses in policy. But that temptation obscures something deeper. The fluctuations themselves may not be anomalies at all—they may be intrinsic to how modern economies function.

This is the intellectual terrain of business cycle theory: a field that asks not merely why crises happen, but why economies oscillate at all.

I first encountered this puzzle while examining a dataset on post-war GDP fluctuations. What struck me was not the severity of downturns, but their recurrence. The intervals varied, the triggers differed, yet the rhythm persisted. That observation—mundane on the surface—forced a reconsideration: perhaps instability is not a deviation from equilibrium, but a feature of it.

What Is Business Cycle Theory?

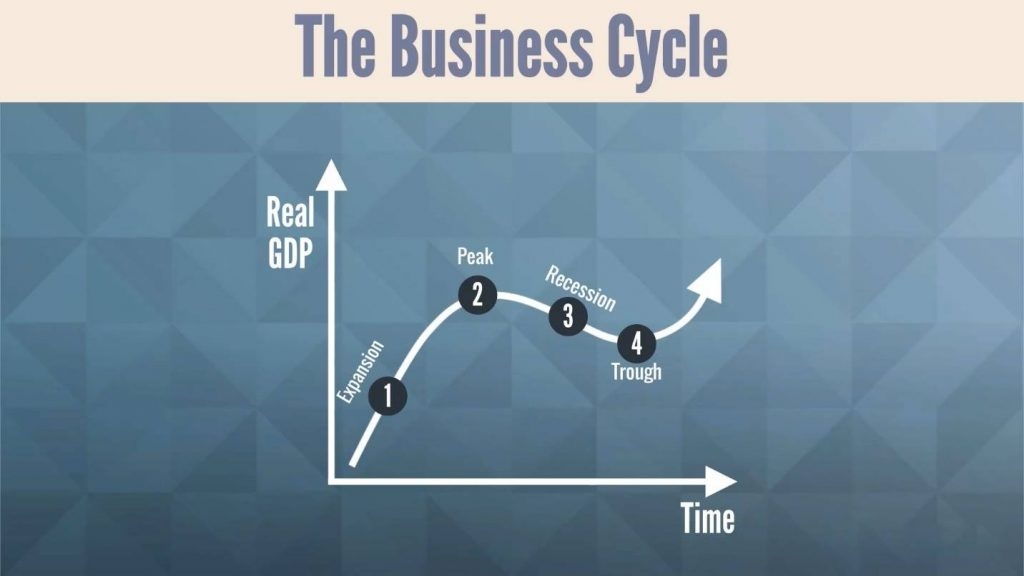

At its core, business cycle theory studies the periodic fluctuations in economic activity—measured through output, employment, investment, and consumption—around a long-term growth trend. These fluctuations are not random. They exhibit phases:

-

Expansion

-

Peak

-

Contraction (or recession)

-

Trough

The question, however, is not descriptive. It is causal. Why do these phases emerge? Why don’t economies simply grow smoothly?

Different schools of thought provide competing answers, each embedding a distinct view of markets, institutions, and human behavior.

Competing Explanations: A Fragmented Intellectual Landscape

Classical and Real Business Cycle Perspectives

The classical tradition, revitalized in the late 20th century through the work of economists like Edward C. Prescott and Finn E. Kydland, treats business cycles as efficient responses to real shocks—particularly technological changes.

In this view, recessions are not failures; they are adjustments. A negative productivity shock reduces output, and rational agents respond by working less and consuming less. The economy is always in equilibrium, even during downturns.

This framework, known as Real Business Cycle (RBC) theory, is elegant. It removes the need for persistent market failures. But it does so at a cost: it struggles to explain the depth of crises or the persistence of unemployment.

Keynesian Interpretations

The Keynesian tradition, rooted in the work of John Maynard Keynes, offers a starkly different narrative. Here, fluctuations arise from demand deficiencies, amplified by rigidities—sticky wages, imperfect information, and coordination failures.

Recessions, in this framework, are not efficient adjustments. They are systemic failures where markets fail to clear. Idle resources coexist with unmet needs, not because of rational optimization, but because of institutional frictions.

Keynesian models emphasize the role of policy—particularly fiscal and monetary interventions—in stabilizing the cycle.

Monetary and Financial Theories

Another strand, associated with economists like Milton Friedman, attributes cycles to monetary disturbances. Fluctuations in the money supply, often driven by central bank actions or banking system dynamics, generate expansions and contractions.

More recent approaches extend this logic into financial markets. Credit booms, leverage cycles, and asset price bubbles become central mechanisms. The financial system is no longer a passive intermediary—it is an active source of instability.

New Synthesis Models

Contemporary macroeconomics attempts to reconcile these perspectives. New Keynesian models incorporate microfoundations and rational expectations—concepts popularized by Robert Lucas Jr.—while retaining nominal rigidities and market imperfections.

The result is a hybrid framework: one that acknowledges both real shocks and demand-side frictions. Yet, even this synthesis remains incomplete. It captures many features of business cycles, but not all.

A Comparative View of Business Cycle Theories

| Theory Type | Key Drivers | View of Recessions | Role of Policy | Core Weakness |

|---|---|---|---|---|

| Classical / RBC | Technology shocks | Efficient adjustments | Minimal | Ignores unemployment persistence |

| Keynesian | Demand shocks, rigidities | Market failure | Active stabilization | May overstate policy effectiveness |

| Monetarist | Money supply fluctuations | Policy-induced instability | Rule-based intervention | Simplifies financial complexity |

| Financial Cycle Theories | Credit and leverage | Systemic fragility | Macroprudential policy | Hard to model precisely |

| New Keynesian Synthesis | Mixed (real + nominal) | Partial inefficiency | Conditional intervention | Still incomplete |

This table reveals less consensus than one might expect. Each framework isolates a mechanism, elevates it, and in doing so, inevitably abstracts from others.

The Role of Expectations: A Subtle but Powerful Force

One of the most consequential insights in business cycle theory is that expectations are not passive—they are generative.

When firms expect future demand to rise, they invest. When households anticipate downturns, they save. These decisions, aggregated across the economy, can validate the very expectations that produced them.

This recursive logic—where beliefs shape outcomes, and outcomes reinforce beliefs—introduces a layer of indeterminacy. Cycles may not require large shocks; small disturbances, amplified through expectations, can suffice.

This is where the elegance of purely mechanical models begins to fray. Human behavior, even when modeled as rational, introduces complexity that resists neat equilibrium narratives.

Institutions and the Shape of Cycles

It is tempting to search for universal laws governing business cycles. But institutions matter—profoundly.

Labor market regulations, financial systems, central bank mandates, and fiscal frameworks all shape how economies respond to shocks. A recession in one country may manifest as a mild slowdown in another, not because the shock differs, but because the institutional response does.

This observation aligns with a broader insight: economic fluctuations are not just about shocks—they are about how societies absorb them.

A Personal Lesson: When Models Meet Reality

During a research project on emerging market volatility, I relied heavily on a standard DSGE (Dynamic Stochastic General Equilibrium) model. The model performed well under normal conditions. It predicted moderate fluctuations, smooth adjustments, and rapid recoveries.

Then came a financial shock.

The model failed—not marginally, but fundamentally. It could not account for the sudden collapse in credit, the sharp contraction in output, or the prolonged stagnation that followed.

That failure was instructive. It revealed that models, no matter how sophisticated, are simplifications. They illuminate certain mechanisms while obscuring others. Business cycle theory is not a single lens—it is a collection of lenses, each distorting reality in its own way.

Are Business Cycles Inevitable?

This question sits at the heart of the debate.

If cycles are driven by real shocks and efficient responses, as RBC theory suggests, then they may be unavoidable. Attempts to smooth them could even be counterproductive.

If, however, cycles are the result of market failures, coordination problems, or policy mistakes, then there is scope for mitigation—perhaps even prevention.

The truth likely lies somewhere in between. Some fluctuations are inevitable. Others are amplified by institutional weaknesses or policy errors.

The Political Economy of Stabilization

Business cycle theory does not operate in a vacuum. Policy responses are shaped by political constraints, institutional credibility, and distributional conflicts.

Consider fiscal stimulus during a recession. In theory, it can boost demand and accelerate recovery. In practice, it raises questions: Who benefits? Who pays? How is it financed?

These questions do not have purely economic answers. They are inherently political.

This intersection—between economic theory and political reality—is where much of the complexity of business cycles resides.

A Provocative Conclusion: Stability Is Not Neutral

There is a tendency to treat economic stability as an unqualified good. But stability, like volatility, has distributional consequences.

Booms create winners—often those with access to capital and information. Busts impose costs—disproportionately on workers and smaller firms. Policies that stabilize the cycle may mitigate these effects, but they also redistribute resources in less visible ways.

So the question is not simply how to eliminate cycles. It is whose interests are served by different patterns of stability and instability.

Business cycle theory, at its best, does not offer definitive answers. It sharpens the questions. It forces us to confront the possibility that economic fluctuations are not just technical problems to be solved, but reflections of deeper structural and institutional choices.

And perhaps that is the most unsettling insight of all: the rhythm of booms and busts is not merely an economic phenomenon. It is a mirror—one that reflects how societies organize production, distribute risk, and respond to uncertainty.

- Arts

- Business

- Computers

- Jogos

- Health

- Início

- Kids and Teens

- Money

- News

- Personal Development

- Recreation

- Regional

- Reference

- Science

- Shopping

- Society

- Sports

- Бизнес

- Деньги

- Дом

- Досуг

- Здоровье

- Игры

- Искусство

- Источники информации

- Компьютеры

- Личное развитие

- Наука

- Новости и СМИ

- Общество

- Покупки

- Спорт

- Страны и регионы

- World