What is My Credit Score?

What is My Credit Score?

Your credit score is more than just a number—it’s a reflection of your financial habits and a key factor that lenders, landlords, and even employers may consider when evaluating your financial responsibility. Understanding what a credit score is and how it works can help you make smarter financial decisions and open doors to better opportunities.

What Exactly is a Credit Score?

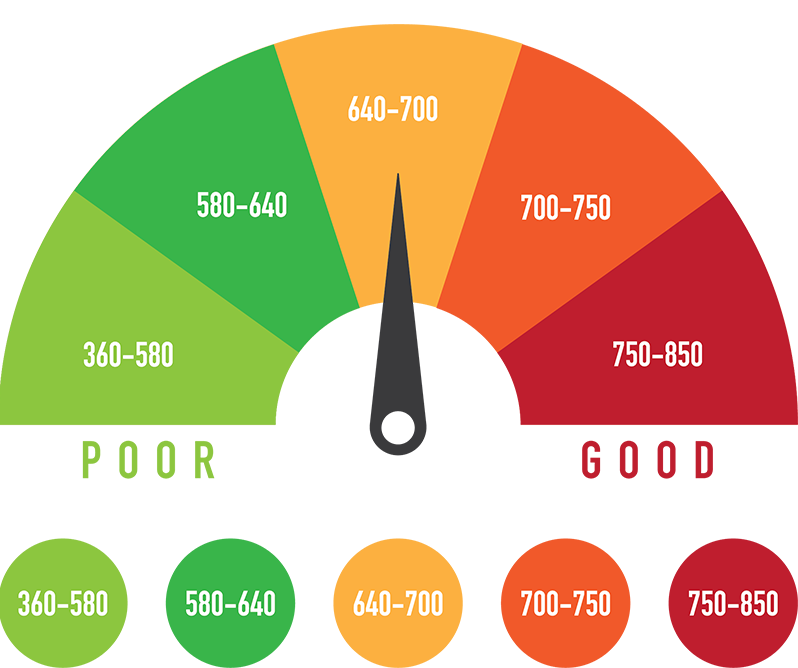

A credit score is a three-digit number, typically ranging from 300 to 850, that summarizes your creditworthiness. Essentially, it tells lenders how likely you are to repay borrowed money. A higher score indicates lower risk, while a lower score suggests higher risk.

Credit scores are calculated based on the information in your credit report, which is a detailed record of your borrowing and repayment history. The most common credit scoring model is the FICO score, though others, like VantageScore, are also widely used.

How is a Credit Score Calculated?

Your credit score is determined by several key factors:

-

Payment History (35%)

Making payments on time consistently boosts your score, while late payments, defaults, or bankruptcies can significantly lower it. -

Amounts Owed (30%)

This looks at your credit utilization—the percentage of available credit you’re using. High balances relative to your limits can hurt your score, even if you pay on time. -

Length of Credit History (15%)

The longer your credit accounts have been open, the more reliable your credit history appears to lenders. Closing old accounts can sometimes lower your score. -

Credit Mix (10%)

A diverse mix of credit types—such as credit cards, installment loans, and mortgages—can positively influence your score, showing you can manage different types of credit responsibly. -

New Credit (10%)

Applying for multiple new accounts in a short period can be seen as risky behavior and may temporarily lower your score.

Why Your Credit Score Matters

Your credit score can affect many aspects of your financial life:

-

Loan Approval and Interest Rates: Higher scores often qualify you for better interest rates and terms.

-

Rental Applications: Landlords may check your score to assess reliability as a tenant.

-

Employment Opportunities: Some employers review credit reports (not scores) for financial positions.

-

Insurance Premiums: Certain insurers use credit-based scores to set rates.

How to Check Your Credit Score

You can check your credit score through:

-

Banks or Credit Card Companies: Many provide free monthly credit score updates.

-

Credit Reporting Agencies: Equifax, Experian, and TransUnion offer credit reports and scores.

-

Third-Party Services: Several apps and websites provide free or paid credit monitoring services.

Checking your own credit score is considered a “soft inquiry” and does not affect your score.

Tips for Improving Your Credit Score

-

Pay bills on time every month.

-

Keep credit card balances low relative to limits.

-

Avoid opening too many new accounts at once.

-

Maintain a mix of credit types responsibly.

-

Regularly review your credit report for errors and dispute inaccuracies.

Frequently Asked Questions (FAQ)

1. What is a good credit score?

A score above 700 is generally considered good, while 800 and above is excellent. Scores below 600 may be considered poor and can make borrowing more expensive.

2. How often should I check my credit score?

It’s recommended to check your credit score at least once a year and monitor it more frequently if you are planning to apply for a loan or mortgage.

3. Does checking my credit score lower it?

No. Checking your own credit score is a soft inquiry and does not impact your score.

4. How long do negative marks stay on my credit report?

Late payments typically stay on your report for 7 years, while bankruptcies can remain for up to 10 years.

5. Can I have more than one credit score?

Yes. Different scoring models exist, so your score may vary slightly depending on which model a lender uses.

6. How long does it take to improve my credit score?

Improvement depends on your situation. Paying bills on time and reducing debt can improve your score in a few months, while rebuilding from serious negatives may take several years.

7. Can I dispute errors on my credit report?

Absolutely. You can contact the credit bureau reporting the error to have it corrected, which can positively affect your score.

Your credit score is a powerful financial tool that can open doors—or close them. By understanding what it is, how it’s calculated, and how to manage it wisely, you can take control of your financial future and make informed decisions that benefit you in the long run.

- Arts

- Business

- Computers

- Spellen

- Health

- Home

- Kids and Teens

- Money

- News

- Personal Development

- Recreation

- Regional

- Reference

- Science

- Shopping

- Society

- Sports

- Бизнес

- Деньги

- Дом

- Досуг

- Здоровье

- Игры

- Искусство

- Источники информации

- Компьютеры

- Личное развитие

- Наука

- Новости и СМИ

- Общество

- Покупки

- Спорт

- Страны и регионы

- World