What is aggregate demand and aggregate supply?

The Economy Is Not a Machine—But We Keep Treating It Like One

I once sat in a policy seminar where a senior official insisted that “demand just needs a push.” He said it the way one might talk about restarting a stalled engine. The room nodded. Charts followed—smooth curves, neat intersections, equilibrium points behaving as if summoned by algebra rather than contested by politics, expectations, and institutional frictions.

I left uneasy. Not because the framework was wrong, but because it was too easily mistaken for something complete.

Aggregate demand and aggregate supply—AD and AS—are among the most enduring constructs in macroeconomics. They promise clarity: a way to compress the sprawling complexity of an economy into two curves and a crossing point. But the elegance hides tension. Beneath those curves lie disagreements about how economies function, how prices adjust, and how governments should act when things go wrong.

This is not just a story about curves. It is a story about coordination, belief, and the uneasy boundary between theory and policy.

What Is Aggregate Demand?

Aggregate demand (AD) represents the total spending on goods and services within an economy at a given overall price level and time period. It is often summarized by a deceptively simple identity:

AD = C + I + G + (X − M)

Consumption, investment, government spending, and net exports. Four components that, together, define the demand side of an entire economy.

But the identity conceals a deeper question: why do these components move the way they do?

The Behavioral Core of AD

Consumption depends on income, but also on expectations about future income. Investment hinges on interest rates, yes—but also on uncertainty, technological opportunities, and institutional credibility. Government spending reflects policy choices, often constrained by political cycles. Net exports respond to exchange rates, global demand, and trade structures.

The AD curve slopes downward—not because of a single mechanism, but because of several overlapping effects:

-

Wealth effect: Lower prices increase real purchasing power.

-

Interest rate effect: Lower prices reduce interest rates, encouraging investment.

-

Exchange rate effect: Lower domestic prices make exports more competitive.

Each mechanism assumes a degree of responsiveness that may or may not exist in reality. In times of crisis, for instance, interest rates can fall without stimulating investment—a reminder that expectations can override mechanical relationships.

What Is Aggregate Supply?

Aggregate supply (AS) captures the total output firms are willing to produce at different price levels. But unlike demand, supply behaves differently across time horizons.

Short-Run vs. Long-Run: A Crucial Distinction

In the short run, prices and wages are sticky. Firms respond to higher prices by increasing production because their costs do not immediately adjust. The short-run aggregate supply (SRAS) curve slopes upward.

In the long run, however, wages and expectations adjust. Output is determined not by prices, but by factors like technology, labor, and capital. The long-run aggregate supply (LRAS) curve is vertical at the economy’s potential output.

This distinction is not merely technical—it reflects a deeper debate about how flexible economies truly are.

The Fragility of “Potential Output”

Potential output is often treated as an anchor, a stable point toward which the economy gravitates. But this stability is more fragile than it appears.

Technological change can shift it. Labor market disruptions can erode it. Policy decisions—education, infrastructure, institutional quality—can reshape it over time.

The long run is not immune to shocks; it simply absorbs them differently.

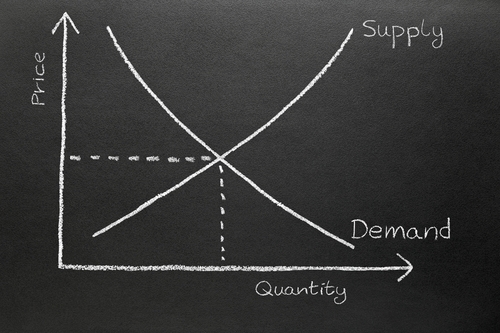

Where AD Meets AS: Equilibrium and Its Discontents

The intersection of AD and AS determines the equilibrium price level and output. It is a powerful visualization—but also a simplification.

In textbooks, equilibrium is clean. In reality, it is contested.

Consider a negative demand shock—a collapse in consumer confidence, for instance. AD shifts left. Output falls. Unemployment rises.

The model suggests a path back: prices adjust, wages fall, and the economy returns to potential output.

But this adjustment can be slow, painful, and incomplete. Workers resist wage cuts. Firms delay hiring. Expectations become self-fulfilling.

Equilibrium, in practice, is not a point—it is a process.

A Comparison That Reveals More Than It Simplifies

| Dimension | Aggregate Demand (AD) | Aggregate Supply (AS) |

|---|---|---|

| Core Definition | Total spending in the economy | Total production/output in the economy |

| Key Components | C + I + G + (X − M) | Labor, capital, technology, institutions |

| Curve Slope | Downward | Upward (short run), vertical (long run) |

| Primary Drivers | Income, expectations, interest rates, fiscal policy | Costs, productivity, expectations, input availability |

| Sensitivity to Policy | Highly responsive to fiscal and monetary changes | More structural; slower response in long run |

| Time Horizon | Mostly short- to medium-term | Short-run (flexible), long-run (capacity constraints) |

| Role of Expectations | Central (consumption, investment decisions) | Central (wage-setting, price-setting behavior) |

| Adjustment Mechanism | Spending changes | Output and price changes |

| Vulnerabilities | Demand shocks, liquidity traps | Supply shocks, productivity stagnation |

This comparison clarifies something often overlooked: AD is more immediately malleable, while AS is more deeply embedded in the structure of the economy.

When Theory Meets Crisis

The distinction between AD and AS becomes most visible during economic crises.

Demand-Driven Recessions

In a demand-driven downturn—such as the global financial crisis—spending collapses. Investment dries up. Consumers retrench.

The policy response typically targets AD:

-

Lower interest rates

-

Fiscal stimulus

-

Liquidity provision

The logic is straightforward: restore demand, and output will follow.

But this assumes that supply remains intact—that firms can ramp up production once demand returns.

Supply Shocks

Supply shocks tell a different story. Consider a sudden increase in energy prices or disruptions in global supply chains.

Here, AS shifts left:

-

Costs rise

-

Output falls

-

Prices increase

This creates a policy dilemma. Stimulating demand may worsen inflation without restoring output.

The AD-AS framework reveals the trade-off—but does not resolve it.

The Quiet Role of Institutions

One lesson I learned the hard way is that AD and AS do not operate in a vacuum. They are shaped—often decisively—by institutions.

Labor market regulations influence wage flexibility. Financial systems determine how quickly investment responds to interest rates. Political stability affects expectations.

In one project, I compared two economies facing similar demand shocks. One recovered quickly; the other stagnated. The difference was not in the curves—it was in the institutions beneath them.

The AD-AS model remained the same. Reality did not.

Expectations: The Invisible Hand Behind the Curves

If there is a single thread connecting aggregate demand and supply, it is expectations.

Consumers spend based on anticipated income. Firms invest based on expected returns. Workers negotiate wages based on expected inflation.

Expectations can stabilize an economy—or destabilize it.

A credible central bank can anchor inflation expectations, making the AS curve more predictable. Conversely, uncertainty can flatten or steepen curves in ways that defy standard assumptions.

The model often treats expectations as exogenous or rational. In practice, they are neither.

Why Policymakers Still Rely on AD-AS

Given its limitations, why does the AD-AS framework persist?

Because it offers a common language.

It allows policymakers, economists, and analysts to communicate complex dynamics in a structured way. It provides intuition, even when precision is elusive.

But reliance on the model can also lead to overconfidence. The curves suggest control—shift demand here, adjust supply there.

Reality is less accommodating.

A Provocation: The Model Is Not the Economy

The enduring appeal of aggregate demand and aggregate supply lies in their simplicity. Two curves, one intersection, a story about balance.

But the economy is not a system that waits patiently for equilibrium. It is shaped by conflict, coordination failures, institutional constraints, and shifting beliefs.

The AD-AS framework captures some of this—but not all.

The risk is not that the model is wrong. The risk is that it is taken too literally.

When policymakers treat demand as something to be “pushed” or supply as something to be “unlocked,” they may overlook the deeper forces at play—trust, incentives, and the architecture of institutions.

The lesson I carried out of that seminar was not to abandon the model, but to resist its seduction.

Aggregate demand and aggregate supply are tools. Useful, even indispensable. But they are not the economy itself.

And confusing the two is where analysis quietly turns into error.

- Arts

- Business

- Computers

- Spiele

- Health

- Startseite

- Kids and Teens

- Geld

- News

- Personal Development

- Recreation

- Regional

- Reference

- Science

- Shopping

- Society

- Sports

- Бизнес

- Деньги

- Дом

- Досуг

- Здоровье

- Игры

- Искусство

- Источники информации

- Компьютеры

- Личное развитие

- Наука

- Новости и СМИ

- Общество

- Покупки

- Спорт

- Страны и регионы

- World